The Lifeline to Your Legal Disputes’ Claim: How this Act Could Be Your Saving Grace

Have you ever wondered if time could run out on a legal claim? The Limitation Act, 1963, answers just that. It answers this question by setting time frames to file a lawsuit, ensuring that justice is pursued promptly.

Whether you’re enforcing a contract, recovering debts, or defending your rights, the Act determines when a claim is valid and when it may no longer stand. In this blog, we’ll break down how this law could impact your legal rights and show you how to navigate the key scenarios where time becomes your biggest challenge.

Imagine facing a claim that’s been around for years—should it still be valid after all that time? This blog will walk you through three scenarios:

- When a claim becomes stale due to time running out (Section 3)

- How courts have the power to excuse certain delays (Section 5)

- When actions of the parties can reset the clock (Section 18)

We want to arm you with practical knowledge so that you’re aware of the deadlines that can affect your rights and how to protect them.

The Limitation Act, 1963, is a backbone of India’s legal system. It sets deadlines for starting various legal actions. Why is this so important? Without deadlines, disputes could drag on forever, making the judicial process chaotic. This Act provides certainty, ensures timeliness, and keeps the system running smoothly by:

- Bringing clarity and closure to legal transactions.

- Preventing parties from delaying legal actions indefinitely.

- Promoting swift resolution of legal disputes.

The Act under Section 3 and Section 5 are the crucial, as they deal with the enforcement of limitation period and possibilities of condoning delays in specific circumstances. On the other hand, Section 18 of the Limitation Act introduces an interesting twist: the clock can be reset based on the conduct of the parties involved.

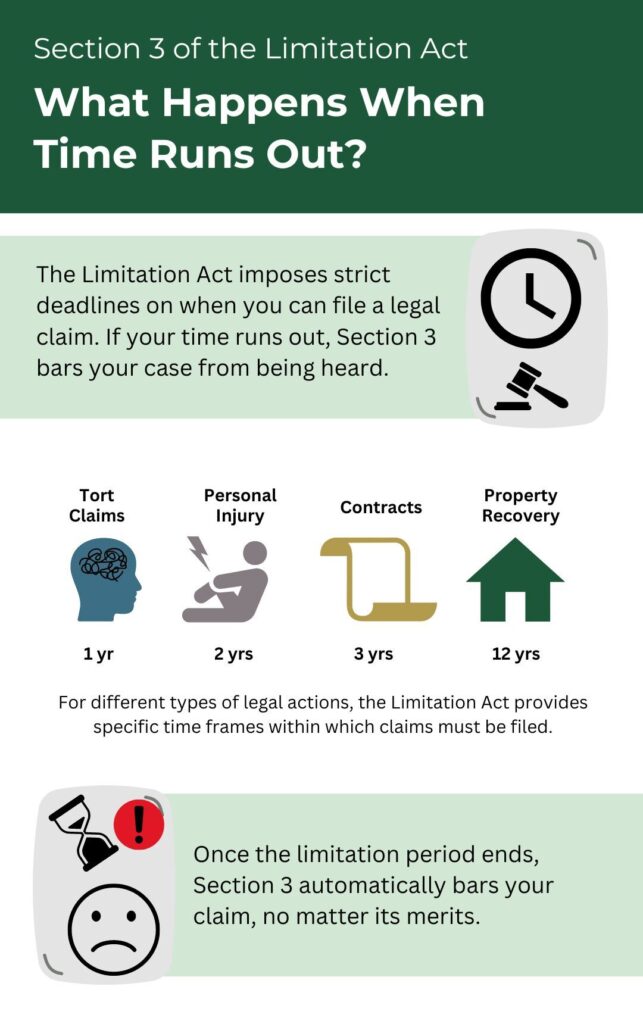

Section 3: Bar of Limitation

Section 3 of the Limitation Act acts as an automatic gatekeeper of time, ensuring that once the clock runs out, the doors to legal action close—whether or not anyone raises the issue. This section applies to all suits, appeals, and applications under civil law, leaving no room for claims filed past the deadline.

The Courts are bound to dismiss such cases on their own, emphasizing the importance of acting within the specific timeframes set by the Limitation Act. By enforcing these deadlines, Section 3 ensures that the judicial system remains efficient and free from the clutter of old, unresolved disputes. It puts everyone on notice: if you’ve got a claim, don’t wait too long, or risk losing your chance to be heard.

The section mandates an automatic bar on lawful actions after the prescribed period. Courts have consistently held that they have a duty, regardless of whether such a defense is raised, to dismiss any suit, appeal, or application filed beyond this timeframe. It applies to all suits, appeals, and applications filed under civil law. There are specific limitation periods provided in the Schedule to the Limitation Act for various types of cases.

Section 5: Saving grace

Section 5 is where the Limitation Act shows a bit of flexibility. While most cases are bound by strict deadlines, this section allows courts to forgive delays in filing appeals or applications—but only if the party can prove they had a “sufficient cause” for missing the deadline. Think of it as a lifeline when unexpected circumstances get in the way of timely action.

Key elements to note:

- Discretion of the Court: Courts have the authority to allow appeals or applications filed late if there’s a legitimate reason, but they decide this on a case-by-case basis.

- Not for Suits: Importantly, Section 5 doesn’t apply to original suits—it’s limited to appeals and applications.

- Burden of Proof: The responsibility to prove “sufficient cause” falls on the party seeking leniency, and each situation is weighed based on its facts.

This section strikes a balance between upholding legal deadlines and delivering justice. It ensures that genuine cases aren’t dismissed simply because someone missed a deadline due to unforeseen events. By giving courts the power to assess exceptional situations, Section 5 recognizes that, sometimes, life just gets in the way and it could be your saving grace.

Section 18: Acknowledgements

Section 18 introduces a strategic safeguard for creditors—if a debtor makes a written acknowledgement that their debt within the prescribed limitation period, the clock resets, offering a fresh window to pursue legal action. Whether it’s a written statement or a payment towards the debt, this acknowledgement breathes new life into a claim that might otherwise have expired.

Here’s why Section 18 matters:

- Resetting the Limitation Period: When a debtor makes an acknowledgement of debt, the limitation period for initiating legal action resets from the date of acknowledgement. This gives creditors a valuable second chance to take a lawful action.

- Timeliness is Key: For this to work, the written acknowledgement must happen within the original limitation period. Once the deadline has passed, no amount of written acknowledgement can bring a claim back to life.

- Proof is Everything: The creditor carries the responsibility of proving that the debtor acknowledged the debt. From signed documents to partial payments, evidence is essential to reset the limitation period. This can include relevant documentation acceptable under the Evidentiary rules covered under the Bharatiya Sakshya Adhiniyam, 2023.

In short, Section 18 is a powerful tool that keeps legal options open, but timing and proof are crucial. It deals with the effect of acknowledgement in writing. Understanding this provision can make all the difference in managing debt-related claims effectively, both for creditors seeking to recover their dues and debtors ensuring they don’t unknowingly restart the clock.

Key Strategies for You: Navigating Debt Acknowledgement with Confidence

Discover how you can effectively manage debt acknowledgement to protect your interests, whether you’re a creditor or debtor! Here are some savvy practices that can benefit you –

Best Practices for Creditors

Secure Written Acknowledgement:

- Always get a written acknowledgement of the debt from the debtor. Remember, verbal acknowledgements won’t reset the limitation period.

- Ensure the acknowledgement is signed by the debtor or their authorized representative.

- Make it a habit to request acknowledgement letters, especially as the end of the limitation period approaches (typically three years for most debts). This simple step can effectively extend your time frame.

Be Clear and Specific:

- Your acknowledgement document should clearly outline the amount owed, the nature of the debt, and the exact terms, including payment schedules and interest rates.

- Use clear, definitive language—avoid vague or conditional statements that could lead to confusion down the line.

Documentation and Record-Keeping:

Keep meticulous records of all written acknowledgements. This includes:

- Letters

- Emails

- Invoices with signed confirmations

- Ensure every acknowledgement is dated and signed by the debtor, and remember: the written acknowledgement must be signed before the limitation period expires to reset the clock.

Regular Follow-Up:

- Periodically follow up with debtors to secure those vital written acknowledgements before the limitation period runs out. This proactive approach helps preserve your legal right to recover the debt.

- Don’t hesitate too long in pursuing legal action, even if you’ve received a written acknowledgement . While Section 18 can be a valuable tool, relying solely on it without timely follow-ups could increase the risk of default.

Professional Drafting:

If the written acknowledgement involves significant sums or intricate arrangements, consider having a legal professional draft the document. This can help minimize ambiguity and disputes over its validity in court.

Best Practices for Debtors

Have you ever wondered if time could run out on a legal claim?

Be Cautious About Signing Acknowledgements

- Know that signing an acknowledgement resets the limitation period, giving creditors more time to take legal action.

- Only sign if the debt is valid, and the amount and terms are clear.

Review Debt Amounts Carefully

Before signing any acknowledgement , review the details carefully:

- Verify the correct debt amount.

- Ensure repayment terms, interest, and penalties are accurate.

- Confirm that any partial payments or reductions are properly reflected.

Use Specific Language to Avoid Confusion

If you intend to dispute a part of the debt, ensure that the written acknowledgement is specific to the undisputed portion. For example, if the debt owed is amount to one lakh rupees, you could state: “I acknowledge owing INR.1,00,000/- but dispute any additional claims.”

Avoid Ambiguous Statements

Do not use vague language or leave the acknowledgement open-ended. This could unintentionally acknowledge more debt than owed or create legal complications.

Consider Negotiation Instead of Acknowledgement

If the creditor requests a written acknowledgement near the end of the limitation period, consider negotiating repayment terms or seeking an amicable settlement rather than signing an acknowledgement that may extend the creditor’s time to sue. You don’t want them to file a lawsuit against you!

Keep a Record of Communications

Maintain copies of all correspondence and documents related to the debt acknowledgement . This can protect you if disputes arise later about what was acknowledged or agreed upon.

Seek Legal Advice Before Signing

If you are unsure about the implications of signing an acknowledgement , always seek legal advice. Lawyers can help ensure that your rights are protected and that you are not unintentionally agreeing to reset the limitation period or acknowledge an incorrect debt amount.

Wrapping Up

In India, Sections 3, 5, and 18 of the Limitation Act, 1963, form the backbone of how legal claims are managed. Section 3 is all about keeping claims timely, while Section 5 steps in as a lifeline for those who may have missed a deadline for valid reasons. Then there’s Section 18, which gives creditors a way to reset the clock through a written acknowledgement of debt—a provision with real weight for both parties involved. Understanding these sections isn’t just useful—it’s crucial for anyone navigating the financial and legal terrain of debt claims.

But with great power comes responsibility. For creditors, this means ensuring their communication is airtight. Clear, well-documented acknowledgement s can be the difference between a smooth recovery process and a complicated legal battle. It’s also essential to have a solid understanding of what courts will accept as proof—after all, the law is only as strong as the evidence backing it up.

For debtors, tread carefully. Even a casual acknowledgement of debt can restart the clock, which may open the door to unexpected financial consequences. Whether intentional or not, acknowledging a debt gives creditors more time to act—so it’s worth consulting with legal counsel to navigate these waters wisely and protect your rights.

In the end, Section 18 is a double-edged sword, balancing the rights of creditors and the protections for debtors. A deeper understanding of how acknowledgement works can empower both sides, ensuring that financial obligations are met fairly and with fewer surprises. More than just a legal provision, it’s a tool that fosters transparency, accountability, and a healthier credit system overall.

FAQs

What is the significance of Section 3 in the Limitation Act for creditors?

Section 3 of the Limitation Act automatically bars a claim if it is not filed within the prescribed limitation period, typically three years for most debts. For creditors, this means that even if the debtor owes money, a delay in filing the suit can lead to the claim being time-barred, preventing legal recovery.

How does Section 5 help creditors when they miss the limitation period?

Section 5 allows creditors to seek condonation of delay for filing appeals or applications if they can show "sufficient cause" for the delay. However, it does not apply to original suits (such as filing a debt recovery suit with a debt recovery agency or others), only to appeals and applications. Courts may extend the limitation period if they find the reason for delay justifiable, such as illness or unforeseen circumstances.

How does Section 18 of the Limitation Act reset the limitation period for debt recovery?

Under Section 18, if the debtor provides a written acknowledgement of the debt, the limitation period resets from the date of the acknowledgement . This gives creditors more time to file a claim and avoid hassle from debt recovery agencies. The acknowledgement must be in writing, signed, and must clearly refer to the debt owed to effectively reset the limitation period.

Can a debtor unintentionally reset the limitation period under Section 18?

Yes, if a debtor acknowledges the debt in writing (even informally, such as via email), the limitation period can be reset under Section 18, even if the debtor did not intend for this to happen. That’s why debtors need to be cautious in making any written statements related to the debt, as it can legally extend the creditor's time to file a lawsuit against you.

What should creditors do to avoid losing their right to recover debt under the Limitation Act?

Creditors should:

- Ensure they file suits within the prescribed limitation period under Section 3.

- Obtain written acknowledgements of debt regularly, particularly before the limitation period expires, to reset the time under Section 18.

- In case of delay, explore the option of applying for condonation under Section 5 for appeals or applications, but remember it won’t apply to original suits.

Nikhil Vasisht

Senior Associate, Dispute Resolution

Nikhil is a senior dispute resolution associate at AKS Law Associates, recognized for his sharp legal insights and dedication to his clients. A graduate of KLE Law College with a master’s from Alliance University, he’s also a passionate reader, drawn to timeless classics like The Idiot by Dostoyevsky.

Thanks for diving into this crucial topic! The Limitation Act, 1963, plays a pivotal role in safeguarding your legal rights. If you’re navigating a dispute or wondering about time limits on a claim, don’t leave questions unanswered. Reach out to our team, and let us guide you through the complexities of this Act.

Leave a comment