Tata Sons vs. Cyrus Mistry: A Corporate Showdown Like No Other

Introduction: When Boardroom Decisions Make Headlines

Have you ever wondered what happens when the leaders of a massive company disagree? What if that disagreement turns into a full-blown legal battle? That happened between Tata Sons, one of India’s most prominent business groups, and its former chairman, Cyrus Mistry.

The fallout between the two wasn’t just another corporate dispute. It became a legal battle that reshaped how companies in India manage leadership changes, protect minority shareholders, and draw the line between business decisions and courtroom interventions. The 2021 Supreme Court verdict didn’t just decide who won and who lost. It set new standards for how companies should operate. Almost everybody across the country followed the story because Tata is a brand that has been a part of the fabric of life in India for more than half a century. The structure of Tata Sons also reflects the nature of countless Indian businesses, large and small, with their origins as a family-owned concern. The outcome of this dispute meant a lot, and not just to those directly involved.

In this blog, you’ll find out what led to this high-stakes battle, what the law says, how the verdict affects businesses, and why it matters to you—whether you’re a law student or a corporate executive.

How Did It All Begin?

Imagine you’re running a family business. Now scale that up to a multi-billion-dollar conglomerate. Taking charge of something on this scale is a massive challenge. In 2012, Tata Sons welcomed Cyrus Mistry as its new chairman. It seemed like a perfect fit. Mistry’s family, through the Shapoorji Pallonji Group, owned 18.4% of Tata Sons, making them the largest minority shareholder, and Mistry had a good track record as the Managing Director of Shapoorji Pallonji Group.

But soon, things went south. Disagreements over significant investments, like those in Corus Steel and Docomo, created friction between Mistry and the Tata board. By October 2016, the board removed Mistry as chairman through a majority vote. This bold move triggered a legal battle lasting almost five years.

What Does the Law Say?

The board cannot remove a chairman on a whim. There are rules to follow. The Companies Act 2013 is like the rulebook for businesses in India. This rulebook played a crucial role in the Tata-Mistry case.

1. Who Gets to Make Big Decisions in a Company?

According to Section 169 of the Companies Act 2013, the board of directors has the ultimate say on leadership roles. In Tata Sons’ case, their internal rulebook—the Articles of Association—didn’t require a special committee to remove a chair. The board’s majority vote was enough.

The Supreme Court agreed. It said courts shouldn’t interfere with business decisions unless there’s a clear legal violation. As long as companies follow their own rules and the law, their business choices are their own.

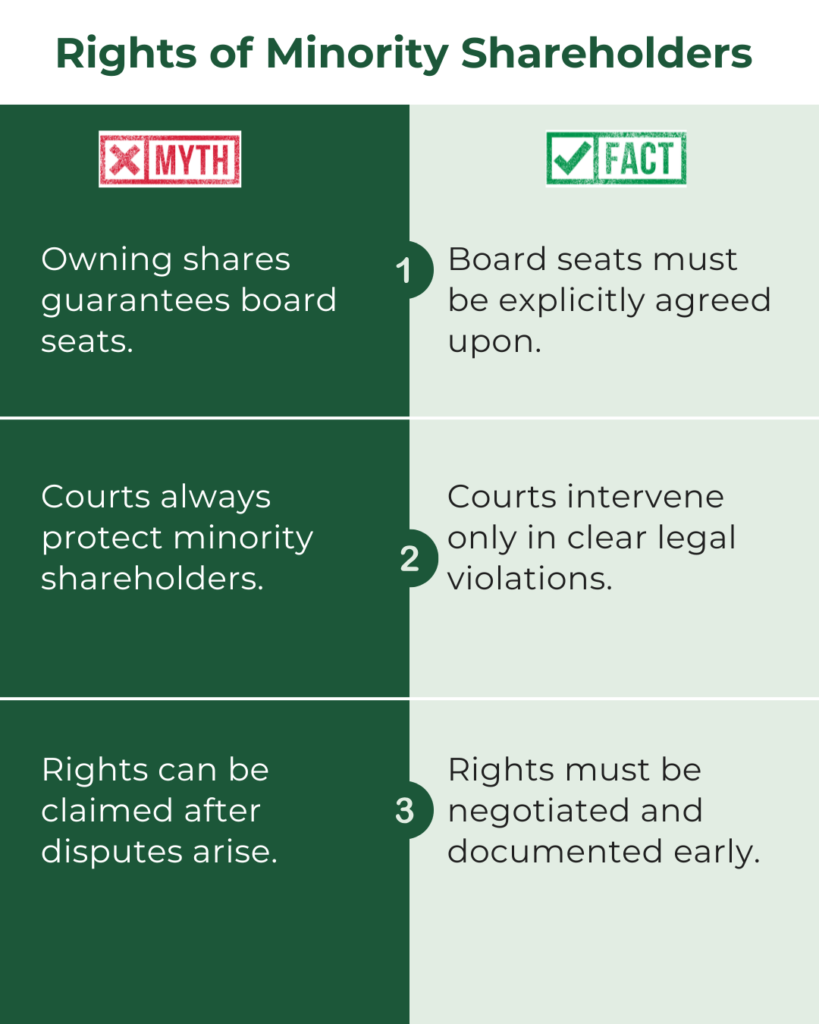

2. What About Minority Shareholders?

Mistry’s family owned a big chunk of Tata Sons. Shouldn’t that give them some power in decision-making? The court didn’t think so. It said minority shareholders don’t automatically get board seats unless it’s written in the company’s rulebook.

It was a wake-up call for minority shareholders: If they want more control, they should negotiate it when they buy shares, not after a dispute starts.

How the Legal Battle Unfolded: The Key Moments

The Beginning: A Leadership Change (2012–2018)

2012: Mistry became Tata Sons chairman.

2016: The board removed Mistry, citing differences in strategy.

2017: Shareholders confirmed his removal in an extraordinary general meeting.

2018: The National Company Law Tribunal (NCLT) sided with Tata Sons, saying the board followed the rules.

The Turning Point: Conflicting Rulings (2019–2021)

2019: Another tribunal, the NCLAT, reversed the earlier decision and reinstated Mistry.

2020: The Supreme Court stepped in and paused the NCLAT’s order, questioning its reasoning.

2021: The Supreme Court made the final call—Tata Sons was right, and Mistry’s removal was valid.

The End: No More Legal Moves (2021–2022)

2022: The Supreme Court dismissed a review petition by the Shapoorji Pallonji Group. The case was closed for good.

What Did the Verdict Mean for Businesses?

1. Business Decisions Stay in the Boardroom

The court affirmed, “We won’t interfere with business strategies unless you break the law.” It was crucial for maintaining trust in boardroom decisions. It helped ensure that companies weren’t dragged to court whenever someone disagreed with a strategy, providing quite a bit of independence for businesses within legal bounds.

2. Minority Shareholders: Negotiate Early or Stay Quiet

If you’re a minority shareholder, don’t wait until a problem arises. The court emphasised the need for firm contracts that spell out your rights. Get it in writing from day one, whether it’s a board seat, veto power, or specific protections.

3. Follow the Rules, Avoid Trouble

The Tata-Mistry case highlighted the importance of following legal and procedural steps. From proper voting processes to clear governance documents, sticking to the rules can save companies from lengthy and costly legal battles. Although the eventual judgement favoured Tata Sons, questions raised by Mistry pointed at possible issues like the lack of proper announcements of the agenda when he was ousted and questions over the meeting minutes. It underscores the importance of meticulously following procedures.

Common Questions You Might Have

Why did Tata Sons win the case?

Tata Sons won as they acted lawfully, followed governance norms, and faced no proven oppression or mismanagement claims.

What does this mean for minority shareholders?

They must negotiate their rights before investing, as statutory protections are limited.

Can a similar case happen again?

Companies now know the importance of transparent governance and legal compliance.

What should companies learn from this?

They should ensure that their governance documents are clear and that decisions follow a proper process.

How does this affect regular shareholders?

It shows that while minority protections exist, they must be well-defined in agreements.

Conclusion: Lessons Learned from the Tata-Mistry Case

The Tata Sons vs. Cyrus Mistry case was more than a corporate fight. It taught companies the importance of balancing power, following rules, and protecting all shareholders.

For law students, this case is a goldmine of legal insights. It demarcates the limits of external oversight into businesses and the importance of following the relevant rule books. It reminds corporate leaders to maintain transparency, fairness, and compliance. The court’s stance was clear: business decisions belong to the Boardroom, not the courtroom.

Tasha Tyagi

Principal Associate, Corporate & Real Estate

With expertise in Corporate Law, Real Estate Law, Commercial Contracts, and Mergers and Acquisitions, Tasha brings a strategic edge to every case she handles. When she’s not advocating for her clients, Tasha can be found experimenting with new recipes inspired by her favourite pastry chefs or immersing herself in the works of Virginia Woolf, Sylvia Plath, or Machiavelli.

Connect with AKS Law Associates today for corporate governance and shareholder rights advice.

Leave a comment