When a Company Defaults: Demystifying the IBC for Everyday Business

Introduction

The Insolvency and Bankruptcy Code (IBC), introduced in 2016, has significantly changed the Country’s approach to handling financial distress in businesses and enterprises. The IBC aims to simplify and speed up the process of resolving insolvencies and bankruptcies, thereby alleviating the companies undergoing financial distress. Initially, the Code was not introduced as a money recovery forum but a forum for resolution and restructuring alike.

At the core of this system is the concept of “default,” which occurs when a company fails to repay its debts. This default triggers the insolvency process under the Code. This blog specifically focuses on Corporate Persons, not Personal Guarantors, who are covered under a separate chapter of the IBC. However, some provisions do apply to both.

The Backstory: Why the IBC was Introduced?

Before the IBC, India had a mix of insolvency laws, including the Sick Industrial Companies Act (SICA), the Recovery of Debts Due to Banks and Financial Institutions Act (RDDBFI), and parts of the Companies Act. Additionally, laws for personal insolvency were scattered, and some chapters in the IBC about personal insolvency are still pending notification. The Legislature felt that these fragmented laws were slow, complex, and often failed to help creditors recover their money. This system led to delays and poor recovery rates, prompting the need for a comprehensive law like the IBC.

Why the IBC Was Needed

The IBC was created to fix several lacunae in the issue that was faced with the fragmented Laws:

- Faster Resolution: Previous laws took too long to resolve insolvency cases.

- Better Credit Discipline: Without a strong insolvency framework, borrowers often ignored their debt obligations, affecting the entire credit system

- Improved Business Environment: A good insolvency system makes it easier to do business, attract investments, and drive economic growth.

- Comprehensive in Nature: IBC is a comprehensive solution, addressing problems faced creditors, subsequent resolution applicants, liquidators, all stakeholders involved with distressed companies.

What is Default under the IBC?

The term “default” is crucial in the IBC because it triggers the insolvency process. Under the Section 3(12) of the IBC, “default” means “non-payment of debt when whole or any part or instalment of the amount of debt has become due and payable and is not repaid by the debtor or the corporate debtor.”

In simpler terms, a default happens when a debtor fails to pay back a debt that is legally due. This can include not only the principal amount but also interest or any portion of the debt, depending on the agreement between the parties.

Therefore, it is not enough for debt to be simply exist; there must also be a “default” for the insolvency process to commence under the Code. Let us take a quick glance at the types of debt, and then dive into its nitty-gritties.

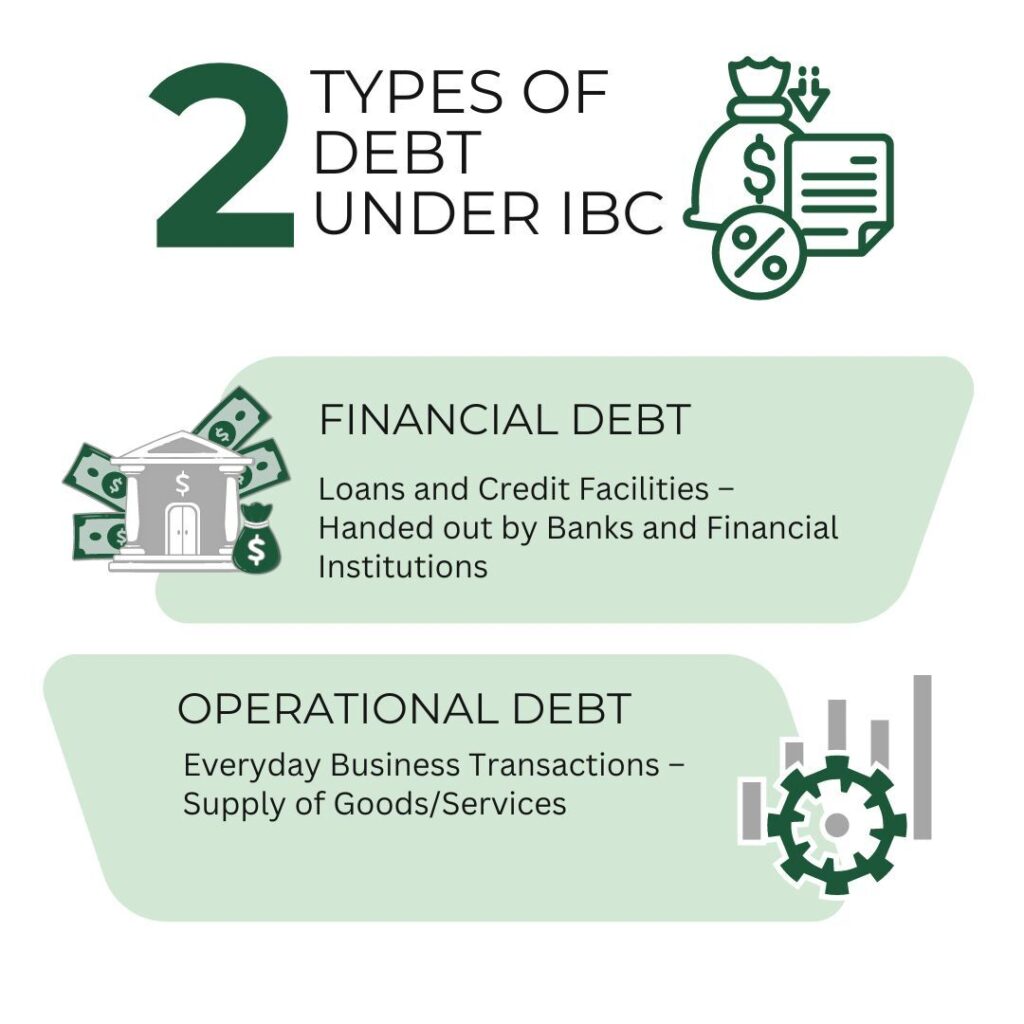

Types of Debt

The IBC deals with two main types of debt:

- Financial Debt: Think of this as the classic loans and credits handed out by banks and financial institutions. These are typically financial transactions, like term loans or working capital loans, where money is the sole focus.

- Operational Debt: This category covers a broader range—debts from the supply of goods or services, employee wages, government dues, or payments owed to local authorities. It’s more about the day-to-day operations that keep businesses running.

When is Debt Due and Payable, Threshold for Default

Now, for the insolvency process to kick in, for the debt must be more than just owed—it must be “due and payable.” Under the Insolvency and Bankruptcy Code, this means that the creditor must be legally entitled to receive the payment, and the payment must be outstanding according to the agreed terms. For example, a loan agreement will specify when payments/interest payments are due. If the borrower fails to make these payments/interest payments, it would then be considered as a Default.

Initially, the IBC allowed insolvency proceedings to be initiated for defaults as low as INR 1 lakh. However, in response to the fallout from COVID-19, the threshold was raised to INR 1 crore. This change aimed to curb a surge of insolvency cases and protect smaller businesses struggling amid the global financial strain.

Why Default Matters

Default under the IBC is important for several reasons:

- Starts the Insolvency Process: A default triggers the Corporate Insolvency Resolution Process (CIRP), providing a clear action point for creditors. The Date of Default, as provided in the Application to initiate such CIRPs, becomes crucial. This date is compared with the contract between the parties to confirm if a default has occurred. It is also checked against the Law of Limitation to ensure that the process is initiated within the legal time frame.

- Promotes Credit Discipline: The threat of insolvency encourages borrowers to repay/settle their debts on time and thus maintain a vibrant, healthy economy.

- Solves NPA Issues: The IBC helps banks and financial institutions deal with Non-Performing Assets (NPAs) by providing a structured way to recover dues. Although it is to be noted that the aspects of NPAs and their restructuring are also governed by the SARFAESI Act. Moreover, RBI Circulars issued from time to time play a role in this process. These circulars, along with the Act, hold statutory value.

Understanding why default matters is crucial, as it serves as the foundation for initiating the resolution process and maintaining financial discipline. With this context in mind, let’s explore how the insolvency process begins and the key players involved in setting it into motion.

Starting the Insolvency Process

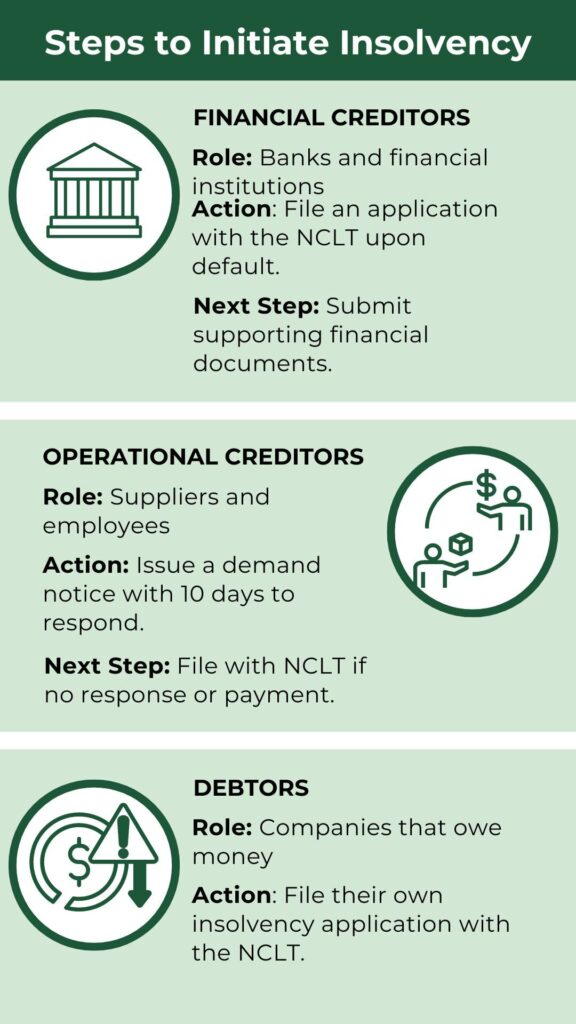

- Financial Creditors

Role: Banks and financial institutions.

Action: Initiate insolvency by filing an application with the NCLT upon default.

Next Step: Provide supporting documents, such as financial records or NeSL records, to prove the debt and default.

- Operational Creditors

Role: Suppliers and employees.

Action: Issue a demand notice to the debtor, allowing at least 10 days for a response.

Next Step: If the debtor doesn’t respond or pay, file an application with the NCLT to start the process.

- Debtors

Role: Companies that owe money.

Action: Initiate their own insolvency process by declaring a default and filing an application with the NCLT.

A Mini Guide to the Insolvency Resolution Process

Once a default is confirmed and the NCLT accepts the application, the process involves several key steps:

1. Leadership during transition – Appointing an Interim Resolution Professional (IRP)

The IRP takes control of the company’s management during the insolvency process. They assess all assets and liabilities and issue an Expression of Interest, inviting interested parties to take over the financially troubled company.

2. Legal Pause – Moratorium Period

During this period, no legal actions can be taken against the company. This allows time to restructure debts and protects the company’s assets, enabling the IRP to evaluate the situation without fluctuations.

3. Decision Makers – Committee of Creditors (CoC)

A group consisting of all financial creditors is formed. They are responsible for deciding on the resolution plan and the next steps for the company undergoing the process, with the ultimate goal of achieving a resolution.

4. Path to recovery – Resolution Plan

The CoC reviews and approves a plan to resolve the company’s financial issues, which may involve restructuring debts or selling assets. This process must be completed within 330 days, subject to any extensions or exemptions provided under the Code. The IBC takes up a time-bound approach for resolution.

5. Liquidation

If no resolution is achieved, the NCLT orders the company to undergo liquidation. Creditors are then paid back according to the “Waterfall Mechanism.”

Some Challenges and Criticisms Along the Way

Despite its benefits, the IBC faces several practical challenges.

Delays: Although the IBC aims for quick resolutions, cases often face delays. This is partly due to legal complexities that arise during the process. The NCLT also struggles with insufficient infrastructure to handle the large volume of cases it receives.

Low Recovery Rates: Creditors often recover less than expected. When a company goes into liquidation, the value of distressed assets can decline, leading to lower recovery amounts than initially projected.

Operational Issues: The NCLT and insolvency professionals sometimes struggle with capacity and efficiency. The involvement of multiple stakeholders can lead to delays and backlogs, complicating the resolution process.

Recent Changes and Developments

The IBC has gone through certain changes to improve its effectiveness and implementation such as:

Threshold Increase: The default threshold was raised to INR 1 crore to protect smaller businesses during the COVID-19 pandemic as stated supra.

Pre-Packaged Insolvency Resolution Process (PIRP): Introduced for the segment/purpose of the MSMEs to provide a faster and cheaper insolvency resolution method.

Group Insolvency Framework: Although not statutorily implemented, there have been working plans being made to address the insolvency of corporate groups. It can help in the coordinated resolution of related companies.

Understanding the Role of the Adjudicating Authority - National Company Law Tribunal (NCLT)

The NCLT, as the Adjudicating Authority, plays a crucial role in the insolvency resolution process under the IBC. It handles insolvency applications, evaluates debt and default issues, ensures the Code is used properly, appoints Interim Resolution Professionals (IRPs), oversees the process, and approves resolution plans. The success of the IBC largely depends on the effectiveness of the NCLT, making it a “need-of-the-hour” to provide the tribunal with adequate resources and skilled personnel to manage the administrative aspects of the Code.

Impact of COVID-19

The pandemic brought significant challenges to the insolvency process. As far as the aspect of Default is concerned, we were introduced with Section 10A of the Code.

Suspension of Proceedings:

During the pandemic, insolvency proceedings for defaults were temporarily suspended to support businesses. This suspension applied from March 25, 2020, to March 25, 2021, meaning defaults occurring during this period could not be used to initiate the CIR Process.

It is important for the Adjudicating Authority to carefully assess whether a default occurred within this suspended period. This makes sure that the Code is not misused for defaults during this timeframe. Consequently, the Date of Default must be determined based on the terms of the agreement between the parties, rather than being arbitrarily chosen by the financial creditor.

Future Outlook

The IBC has made significant progress but needs ongoing improvements. Some are –

Strengthening the NCLT: Enhancing the NCLT’s capacity is crucial for ensuring timely resolutions. Expanding the number of courtrooms and halls will help effectively manage the vast number of cases brought before these forums.

Training Insolvency Professionals: Improved training programs for Insolvency Resolution Professionals will elevate the quality of the insolvency process.

Upholding the Code’s Spirit: The IBC was introduced with a noble intent and should not be misused for mere debt recovery or to pressure companies into the CIRP process for motives that fall outside the legislative purpose of the Code.

FAQs

1. What are the four pillars of IBC?

Four Pillars of IBC are –

- Insolvency Professional

- Information Utility

- Adjudicating Authority

- Insolvency and Bankruptcy Board – Regulator

2. What constitutes default under insolvency and bankruptcy code 2016?

Default under IBC would mean the non-payment of debt when whole or any part or instalment of the amount of debt has become due and payable and is not repaid by the debtor or the corporate debtor.

3. Why is IBC a code and not an Act?

The Insolvency and Bankruptcy Code is a code and not an act as it is a combination of various existing laws dealing with insolvency and bankruptcy laws.

4. What is the regulatory body of IBC?

The regulatory body under the IBC is the Adjudicating Authority and the Insolvency and Bankruptcy Board of India

Conclusion

The concept of default under the IBC is a crucial trigger for initiating the insolvency process. By clearly defining default as the non-payment of due and payable debt, the IBC establishes a straightforward criterion for creditors and debtors. This approach also helps weed out frivolous petitions, saving valuable judicial time.

It is essential for the NCLT, as the Adjudicating Authority, to exercise careful scrutiny in summary proceedings. This ensures that a financially healthy company isn’t unnecessarily subjected to the rigors of CIRP, even when a debt and default exist. The applicant must prove the debt and default beyond a reasonable doubt before the NCLT.

While the IBC has succeeded in certain areas, challenges remain. These include delays, the misuse of the Code as a debt recovery tool, threats to otherwise healthy companies, and low recovery rates due to the sale of distressed assets at lower prices.

The IBC must continue to evolve, shaped by practical experience and judicial interpretation, to remain an effective tool for resolving financial distress and supporting economic growth.

Srihari S

Senior Principal Associate, Dispute Resolution

Srihari S is a graduate of OP Jindal University’s Jindal Global Law School and will soon mark five years in legal practice. Specializing in arbitration within commercial construction contracts and Insolvency and Bankruptcy laws, Srihari brings a keen analytical mind to his work. Beyond his legal expertise, he enjoys playing golf, discovering new music, indulging in acrylic and oil painting, and immersing himself in the world of computer gaming.

Disclaimer

This article is intended for general informational purposes and does not constitute legal advice. The same shall not be construed or interpreted as soliciting or advertisement in any manner whatsoever.

Navigating the intricacies of the Insolvency and Bankruptcy Code can be challenging for businesses facing financial distress. Whether you’re a creditor, debtor, or legal advisor, understanding the nuances of default and the insolvency process is crucial. If you have questions or need expert guidance on how to manage or initiate the insolvency process, we’re here to assist you. Contact us to ensure that your actions are compliant, strategically planned, and aligned with the latest developments under the IBC.

Leave a comment